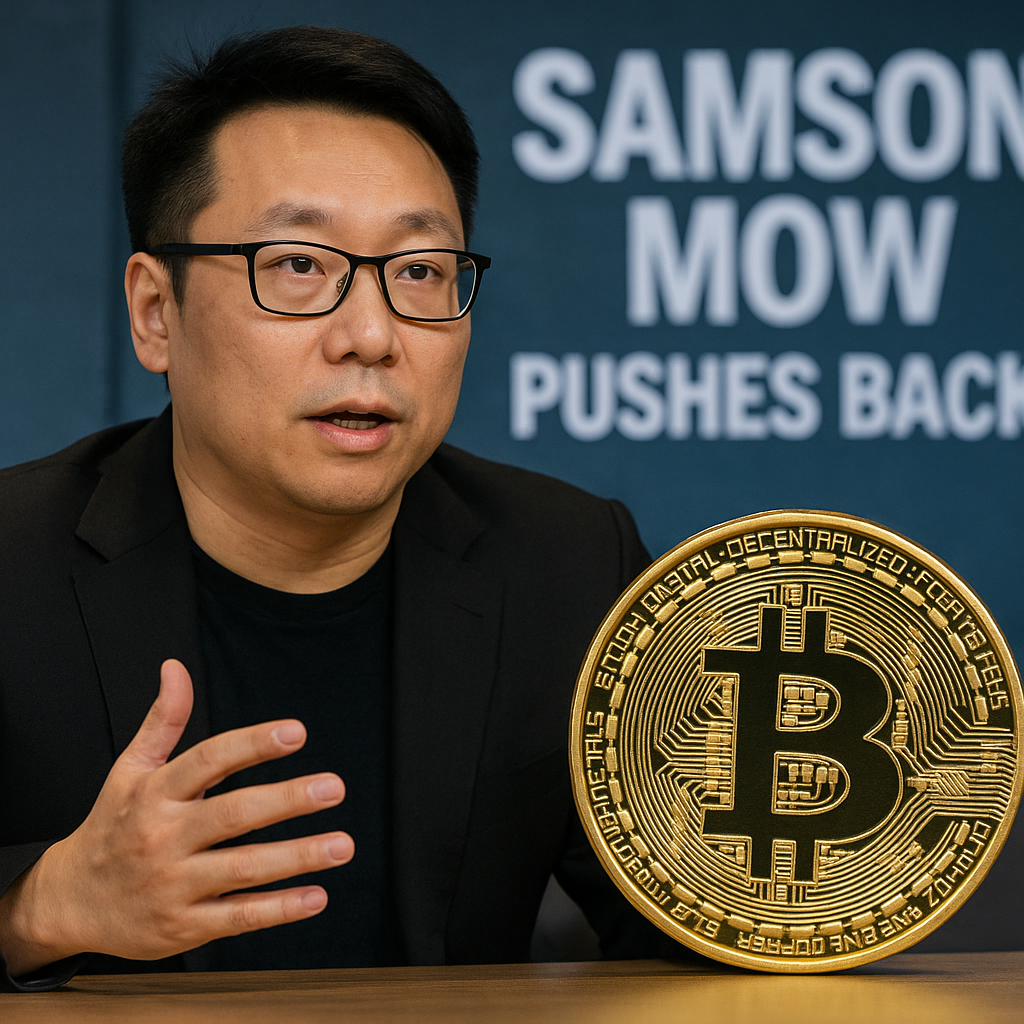

Samson Mow, a prominent Bitcoin supporter, has addressed concerns that Strategy has compromised its values by indicating it may sell BTC in the future to distribute dividends. In a post on X dated May 7, Mow contended that public firms holding BTC require flexibility to safeguard shareholder interests, even if that entails liquidating portions of their holdings at strategic times. According to the JAN3 CEO, the principle of ‘never sell’ was meant for individual investors, not a strict corporate policy. ‘As a personal HODLer, selling Bitcoin without reason is not advisable. The message is to avoid selling if possible, but it doesn’t mean one should hold onto it forever,’ he stated. Mow emphasized that the situation differs for publicly traded treasury companies, urging that a firm’s philosophy should revolve around optionality. He cautioned that a company proclaiming it will only acquire Bitcoin essentially hands a tactical advantage to short sellers and arbitrageurs. Thus, by maintaining multiple strategic options, Strategy can thwart potential adversaries. ‘A well-equipped company is difficult to manipulate; it might sell, hedge, issue new stock, or purchase more,’ he explained. Mow reiterated that Strategy’s primary objective should not be to completely avoid selling Bitcoin but to ensure the benefits and protection of its shareholders. He cited his previous efforts in designing Bitcoin bonds, allowing issuers scheduled Bitcoin sales to return capital to bondholders post-lockup. Without such a framework, he noted that the financial instrument would be unviable. Mow also compared this to Strategy’s STRC preferred stock, which aims to mitigate Bitcoin’s volatility while offering investors asymmetric exposure without the typical downturns. He highlighted a statement from executive chairman Michael Saylor, who noted that Strategy’s Bitcoin breakeven annual return rate stands at approximately 2.05%. This implies that if Bitcoin appreciates beyond this threshold, the company can meet its dividend obligations by selling without adversely affecting shareholder equity. When a user on X suggested that Saylor should face scrutiny due to his ‘never sell’ assertion, Mow bluntly countered that corporate strategy cannot rely on catchy phrases. The dialogue has intensified in light of Strategy’s increasing reliance on preferred stock, especially STRC. In its Q1 2026 financial report, which revealed a substantial loss of $12.5 billion, Strategy disclosed that STRC issuance had reached $8.5 billion, with nearly $12 billion raised this year. Nonetheless, skeptics argue that the company’s model may be overly reliant on generating new securities, with Bitcoin commentator Peter Schiff recently labeling STRC as a ‘clear Ponzi scheme’ and asserting that the firm lacks sufficient operational income beyond its software segment to sustain dividend payouts.